Cart

0

Sign In

My Account

Home

Management Accounting

Charities

Daybooks

Software

Contact

Shop

Sign In

My Account

Cart

0

Home

Management Accounting

Charities

Daybooks

Software

Contact

Shop

Category

All

Coming Soon

Excel

VAT

Currently unavailable

Excel Spreadsheet: Daybooks

£60.00

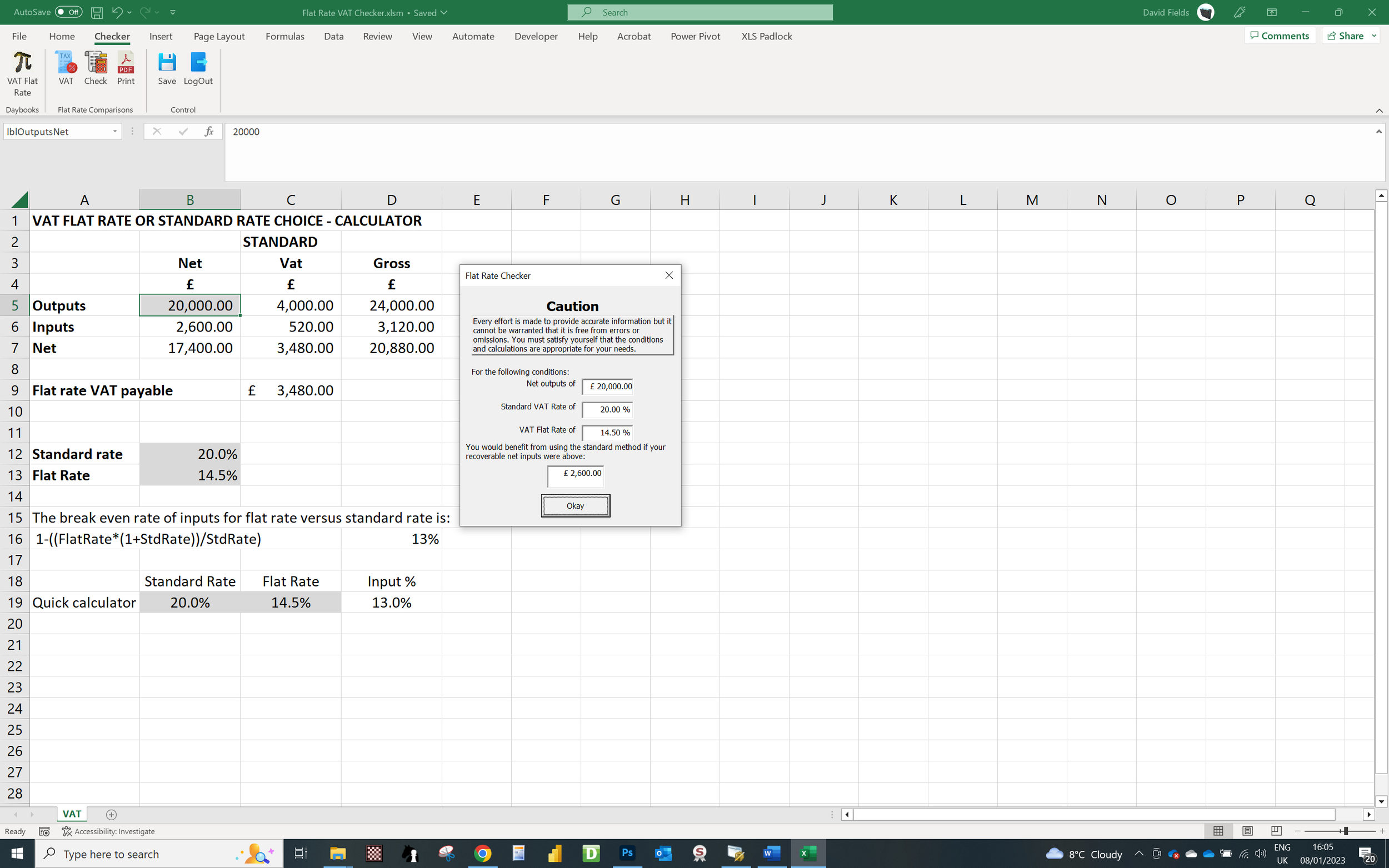

Excel Spreadsheet: VAT Flat Rate Checker

£3.00

Excel Spreadsheet: Management Accounting from SAGE via ODBC

£0.00

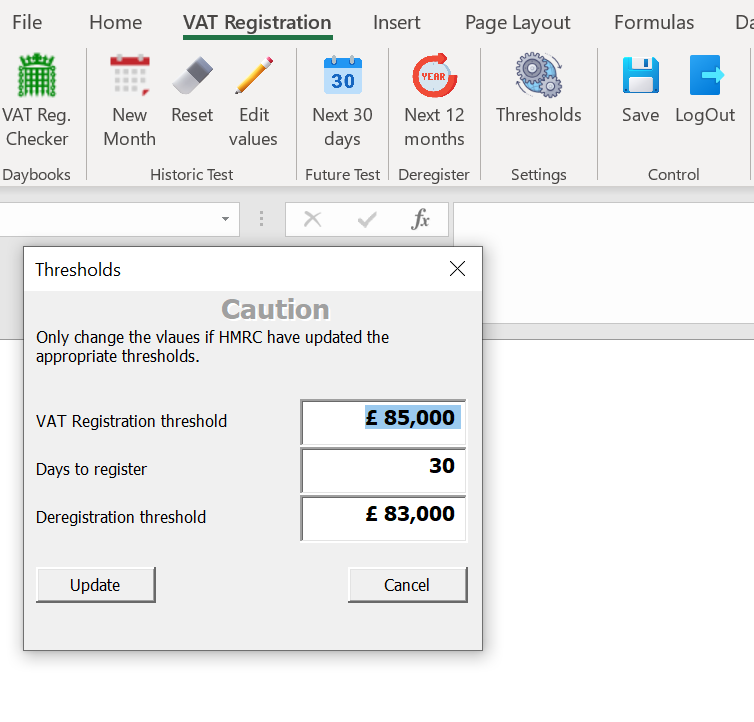

Excel Spreadsheet: VAT Registration Threshold Checker

£3.00

Excel Spreadsheet: VAT 652 Error Reporting

£3.00

Currently unavailable

Excel Spreadsheet: Financial Planning and Analytics

£300.00

Currently unavailable

Excel Spreadsheet: Receipts and Payments Account

£30.00

Currently unavailable

Excel Spreadsheet: Bank Import - Data mapping and transformation

£120.00